MAX Credit Union Partners with Arkatechture to Create Truly Personalized Member Experiences4/7/2022  Lynette Cupps Lynette Cupps Arkatechture, a technology company dedicated to empowering organizations with a better understanding of their business through data, has partnered with MAX Credit Union to leverage Arkatechture’s data analytics platform: Arkalytics. This platform provides a fully managed, cloud-hosted data lakehouse plus its suite of financial reports and executive dashboards for advanced analysis and reporting. This partnership became official in the third quarter of 2021.

According to Lynette Cupps, MAX Credit Union’s SVP of Growth and Innovation, what prompted the credit union to switch to a much more hands-on, fully-managed implementation process like Arkalytics was creating truly personalized experiences for MAX’s members. This personalized experience allows MAX to easily understand member needs through data. Previously, at the credit union, several disparate sources of data made it difficult to understand the member holistically and almost impossible to do it in a timely manner. Cupps says the credit union expects to have better access to member data to be used to deepen relationships and improve the experiences. For the organization, she and her team are looking forward to consolidating duplicate data sources and having one access point for all business lines. “The implementation process of Arkalytics was phenomenal,” Cupps adds. “The implementation team even reprioritized the order of implementation to accommodate an urgent request.” “MAX Credit Union has a team of dedicated and data-driven individuals who know how to get the job done,” states Arkatechture Data Visualization Analyst Brandon Sowell. “Their implementation could not have gone as well as it did if their team wasn't thorough, timely, and prepared at every point of the project. It was a pleasure to work with them on this project.” “The people at MAX Credit Union are a pleasure to work with; they cruised through their Arkalytics implementation,” states Jamie Jackson, Founder & CEO Arkatechture. “They are open about their current challenges, which makes it easier for us to enable them to achieve their goals through analytics. We’re excited about their shared passion for data and how we can be a continued partner for them throughout their data journey today and into the future.”

0 Comments

Joan Opp Joan Opp Stanford Federal Credit Union, comprised of members from the Stanford University community and technology companies in the Bay Area such as Google and Meta, announced that effective April 1, it has discontinued non-sufficient funds (NSF) fees in its ongoing efforts to find new ways to give back to its members.

“Stanford FCU is dedicated to improving the financial lives of our members by offering as much value as possible. Over the past five years we have refunded over $2.3 million in fees to our members,” noted Stanford FCU President & Chief Executive Officer Joan Opp. Opp continued, “Our total fee income is only 2% of our income compared to an average 8% of other financial institutions, and the NSF Fee is one of the few fees left to eliminate.” Stanford FCU is also revising their entire overdraft protection program to further benefit its members, slated to go into effect in the coming months. The new program will enable members to opt-in to decide whether the credit union should pay for items if their account balance is insufficient. If a member opts-in to the new program, it will pay for checking, ACH and debit card purchases should an account go into a zero or negative balance. For transactions under $25, the charge will be paid with no overdraft fee. For purchases of $25 or more, the program will cover the cost of the charge, and the member will be charged a $25 fee. The new program will limit overdraft coverage to three transactions. Stanford FCU also allows members to link their checking account to one other account such as a savings account. This service moves money from the savings to the checking account without a fee, should the member’s account accidentally go negative. Opp commented, “We have never charged members an Account Transfer fee, unlike what many financial institutions have been doing for years.” For more information about Stanford FCU and its latest member offerings, visit sfcu.org.  ValleyStar RISE Foundation Golf Tournament will support Carilion Children's Hospital. ValleyStar RISE Foundation Golf Tournament will support Carilion Children's Hospital. The ValleyStar RISE Foundation, which is the charitable arm of ValleyStar Credit Union, will host a golf tournament on May 5, 2022, at Chatmoss Country Club in Martinsville, Virginia to support Carilion Children’s Hospital located in Roanoke, Virginia.

All funds raised at the golf tournament will support the purchase of life-saving medical equipment at Carilion Children’s Hospital. Each year, the hospital treats more than 40,000 children from 40 counties in Virginia and neighboring states. “It has been two years since we have hosted a golf tournament to support Carilion, and I’m excited to be back,” said Stephanie Potter, Golf Tournament Chair of the ValleyStar RISE Foundation. “I am equally excited that ValleyStar Credit Union’s branches and Contact Center team members will be collecting donations starting now through May 5 for Children’s Miracle Network. These funds will support Carilion Children’s, UVA Children’s, and Children’s Hospital of Richmond at VCU. CMNH is near and dear to our hearts.” Headquartered in Martinsville, Virginia, the ValleyStar RISE Foundation was formed in 2019 and recently received its 501c3 designation in January 2022. The foundation strives to bridge gaps in workforce development and mental and physical health by providing funding as well as volunteer opportunities for ValleyStar Credit Union’s team and board members to happily give their time and talent to support good work in the community. For more information, visit www.valleystar.org/golf.  Paolo Teotino Paolo Teotino To meet growing demand by credit unions for cloud-based data analytics, Trellance is announcing the release of five new cloud offerings. 65% of credit unions have either invested in, or plan to invest and implement cloud-based solutions, according to a recent Cornerstone Advisors survey.

Trellance’s new cloud-based business analytics offerings are available by monthly subscription and include:

Trellance now supports the three leading core systems, Episys, Keystone, and DNA, enabling core data from these systems to be pulled directly into Trellance’s cloud-based descriptive and predictive analytics platform for data analysis and business intelligence. This decreases the costs and efforts required by credit unions to transform data into valuable information, while streamlining data integration and scalability efforts. The native cloud technologies in the Trellance business analytics suite leverage artificial intelligence to identify patterns and suggest actionable insights. With AI-derived precision, it formulates strategies to reduce member attrition, identify clusters of behavior across members and suggest the most appropriate product based on each member’s unique experience with the credit union. “Since the launch of our cloud platform in the fall of 2020, we have seen a surge in cloud propensity from credit unions of all sizes,” said Paolo Teotino, Trellance’s chief product officer. “With our latest cloud offering, we are democratizing credit union access to business analytics and artificial intelligence by offering it ‘as-a-service.’ The cloud technology makes it increasingly possible for credit unions to act faster, better utilize data, drive optimal business decisions very cost-effectively.” Centra Credit Union AVP of Business Analytics Carrie Jenkins said CCU has recently entered into an agreement with Trellance to migrate their existing on-prem M360 platform to the cloud. “Not having to maintain hardware frees up resources that we can reinvest into getting the most out of the analytics applications provided by Trellance,” Jenkins said. In addition to CCU, other credit unions that recently signed contracts to leverage the Trellance cloud platform include:

As Trellance has increased its offerings in the cloud, the company has also further strengthened its cloud security posture. It recently obtained the Cloud Security Alliance’s STAR (Security, Trust, Assurance, and Risk) Registry Level 2 certification, which requires a rigorous third-party independent assessment and meets the highest security requirements in the financial industry. Trellance is also compliant with SOC 1 and 2 standards and is a Level 1 Service Provider certified with the Payment Card Industry Data Security Standard. As Trellance continues to add credit unions to its new cloud platform, it still plans to support credit unions with on-premise infrastructure.  Steve Castagna Steve Castagna AKUVO, a technology-based organization specializing in credit risk and delinquency management, announced today that two new credit unions have signed on to its Aperture platform. They are $498M OnPath Federal Credit Union headquartered in Harahan, La., and $98M Trius Federal Credit Union based in Kearney, Neb.

AKUVO had previously signed five new credit union clients, all with more than $1 billion in assets. These new mid-sized credit unions demonstrate the Aperture platform’s ability to scale performance and accessibility for all asset sizes. Now with seven clients signed so far in 2022, AKUVO is poised for strong, ongoing growth this year. Serving Southwest Louisiana, OnPath FCU was looking for a collections platform that could support its mission of investing in personal relationships through a service-first approach. The OnPath FCU team was immediately drawn to the system’s clean design which enables collectors to get a quick, but complete, view of the account and relationship prior to initiating contact. Additionally, the open API platform’s ability to integrate with other systems increases collector efficiency, enhances the member’s experience, and increases the likelihood of a promise or payment. “We are highly impressed with the team at AKUVO. Their passion for finding innovative ways to leverage data science to help credit unions achieve goals is very exciting and contagious,” said Candace Washington, Vice President of Member Engagement at OnPath FCU. “We’re excited about how we can use Aperture technology to provide individualized delinquency solutions to our members that benefit everyone.” As part of its growth strategy, Trius FCU was looking for a collection platform that could improve efficiency and effectiveness using tools like automation and behavior analytics. Trius was impressed with Aperture’s ability to integrate with other systems and use data to present member insights to help collectors cure accounts more quickly. “Our collectors can focus and really listen to members, providing the human side of service, while Aperture does the rest, using data from our credit union and other sources to cure accounts in a way that reduces loss and retains member loyalty,” said Amy Schade, Vice President of Lending at Trius FCU. “We are excited that these two, great credit unions put their trust in AKUVO,” said Steve Castagna, AKUVO Chief Operating Officer. “Our vision is to provide financial institutions of all asset sizes with tools that allow them to better manage credit risk through efficiency, automation and the power of data science.”  Jack Lynch Jack Lynch PSCU, the nation’s premier payments credit union service organization (CUSO), today announced it is partnering with Q6 Cyber, a leading provider of e-crime intelligence for financial institutions worldwide, to better identify and respond to advanced cyber threats and fraud activity with greater speed, accuracy and effectiveness.

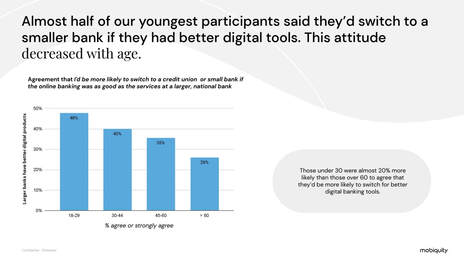

“Every year, Q6 Cyber identifies millions of hacked or compromised financial accounts, enabling our clients to preempt account takeover and fraud, while also substantially reducing payment card fraud by up to 50% year over year,” said Eli Dominitz, CEO at Q6 Cyber. “We look forward to working with PSCU to deliver these types of results to the CUSO’s Owner credit unions and their members to help them stay ahead of and combat cybercrime.” Q6 Cyber will collect information from multiple sources, then analyze and correlate it to provide targeted, valuable and actionable intelligence to proactively disrupt cybercriminal and fraudulent activity directed toward PSCU, its Owner credit unions and their members. Additional services Q6 Cyber will provide include detection of mule accounts, Dark Web monitoring and analysis of compromised employee credentials. “As we saw in PSCU’s 2021 Eye on Payments study, consumers are increasingly gravitating to digital and online experiences, leading to an increase in e-commerce and online transactions, which is in turn driving online fraud numbers even higher,” said Jack Lynch, chief risk officer at PSCU. “Our partnership with Q6 Cyber is primed to position PSCU to best help our Owner credit unions and their members combat cybercrimes, with a goal of stopping these types of fraudulent activities before they can even occur.” PSCU employs a connected approach to combat fraud, utilizing a number of technologies and best practices to block fraud at the point of sale, in the contact center and online, among other channels – while delivering an enhanced cardholder experience. This includes PSCU’s proprietary Linked Analysis, developed by PSCU’s in-house fraud experts to prevent fraud before it happens by leveraging cross-network analytics. In fiscal year 2021, the CUSO stopped nearly $500 million in fraudulent transactions for its Owner credit unions and their members. In addition, PSCU’s Enhanced Fraud Services addresses fraud concerns for credit unions with unique characteristics in their membership portfolio that require a customized approach. Credit unions receive an assigned risk program consultant who, on a daily basis, holistically analyzes the credit union’s fraud and risk mitigation initiatives. From there, risk program consultants build a customized program and response plan, which helps strengthen a credit union’s existing anti-fraud efforts in order to more quickly and accurately prevent fraud and reduce losses.  Mobiquity, a digital consultancy that designs and delivers innovative digital products and services for the world's leading brands, released today results of The Digital Opportunity for Credit Unions Report. This report showcases an opportunity for smaller institutions and community banks to compete with their larger rivals and increase market share by adopting digital tools. Mobiquity surveyed over 1,000 customers ages 18 and up in the U.S. to uncover generational banking behaviors, satisfaction levels based on where customers bank and what would encourage more consumers to bank at credit unions.

According to Mobiquity’s findings, how customers rank their ideal banking experience is greatly impacted by digital accessibility. Currently, satisfaction is highest among those who bank at credit unions and community banks for their primary banking needs, particularly among customers over the age of 45. While large banks are the most popular choice (45%), almost a quarter (24%) of respondents bank at credit unions and do so because of the great customer service—especially for those aged 60+ of whom 70% rank this value in their top three. For younger generations, both easy-to-use digital tools and having a wide range of digital options continue to be top factors for their ideal banking experience. However, these same younger customers strongly agree they would be more likely to switch to a credit union or small bank if the online banking was as good as the services at a larger, national bank (50%). “It’s no surprise that the digital experience continues to be a driving force for customers when choosing a banking institution,” said Matt Williamson, VP of Global Financial Services at Mobiquity. “Our latest Digital Opportunity for Credit Unions Report found that those who are currently banking at credit unions do so because of the community feel and level of customer service. If credit unions can master converting that same feeling and connection of customer service into a digital banking experience, they have the potential to capture the business of younger generations and those to come.” Additional key findings include:

The full copy of The Digital Opportunity for Credit Unions Report is available at https://www.mobiquity.com/credit-union-trends-research. If you are interested in learning more about how Mobiquity is quickly transforming companies’ digital strategies, see here: https://www.mobiquity.com/our-work  Jim Ryan Jim Ryan Curql Collective (curql.com) is pleased to announce the appointment of Jim Ryan as Vice President of Strategic Partnerships. In his role, Ryan will assist the President & CEO in leading key top-tier partnerships at Curql Collective, including managing key partnerships with fintech, credit unions, the Curql Fund manager, and other key industry stakeholders. Ryan will formulate new and support existing business strategies, develop and manage strategic partnerships, and lead projects.

Prior to joining Curql Collective Ryan served as President of Financial Center Services, LLC., the wholly-owned CUSO of Financial Center First Credit Union (FCFCU) in Indianapolis, IN where he led the overall organization, direction, control, and evaluation of CUSO operations, partnerships, and investments. At FCFCU, Ryan managed the credit union’s Centralized Sales Team, including business development, investment services, and the centralized lending area. “Jim is an experienced credit union executive well known for his success developing and leading high-performing teams,” says Nick Evens, President & CEO of Curql Collective. “We are very excited to add such an accomplished relationship builder to the team, and look forward to the growth we will see in the coming years.”  First Financial Federal Credit Union is pleased to announce its merger with Wor-Co Federal Credit Union, an education-based credit union on the Eastern Shore of Maryland. The merger was completed on March 22, 2022.

Wor-Co Federal Credit Union served the Somerset and Worcester Public School systems as well as several businesses, and healthcare facilities in the area. “We are excited for the opportunities this merger brings to the former Wor-Co members. First Financial offers a variety of financial products, convenient services, and the personal service our members have come to expect from their credit union,” stated Dawn White, Wor-Co FCU Supervisory Committee Chair. As a result of the merger, First Financial now serves four school systems throughout Maryland, and over 90 select employer groups within their service region. “Having the common bond as education-based credit unions, the merger between First Financial and Wor-Co is a very natural fit,” said Eric Church, First Financial FCU President/CEO. “We are excited to welcome aboard the members of Wor-Co Federal Credit Union, and look forward to being a part of their community.” CuneXus Named a 2022 Banking Technology Awards Finalist for its Superior Digital Storefront4/1/2022  Dave Buerger Dave Buerger CuneXus, the first and only digital storefront for financial institutions’ account holders, today announced that they were named a finalist for the Fintech Futures Banking Technology USA Awards for their innovative, first-to-market Digital Storefront.

The CuneXus Digital Storefront reinvents the way financial institutions approach consumer lending by delivering tailored financial products and services that are preapproved with one-click convenience. Account holders can log on to online banking, view their personalized, easy-to-use menu of guaranteed offers and select what best suits their needs. For lenders, this storefront can improve their cross-sell and marketing capabilities to further enhance communication and focus on deepening their customer relationships. CuneXus continues to set the standard for digital lending by providing technology to credit unions and banks across the country to meet their consumer needs. The digital storefront has helped the largest lenders in the U.S. execute new account holder acquisition, grow non-interest income, and create sales enabled branches. In addition to the robust, menu-based storefront, CuneXus fully eliminates the dated credit application process. “We are thrilled to be considered as a finalist for the Banking Tech USA Awards for the Best Consumer Digital Banking Solutions Provider,” said Co-Founder and President, Dave Buerger. “The digital storefront was developed to ensure that consumers have access to the funds they want in their moment of need, and lenders can benefit from efficiencies that boost their bottom line. We are always striving to help financial institutions exceed consumer expectations through technology like no other; and this Storefront is only proof of this dedication.” Winners will be announced at a gala dinner ceremony at the Julia Morgan Ballroom in San Francisco on May 19, 2022. More on the awards can be found here: https://informaconnect.com/banking-tech-awards-usa/the-shortlist/ |

Author: Mike LawsonMarried to a most gorgeous and wonderful wife, raising 5 kiddos (including twins!), enjoy helping others tell their stories, and love surfing SoCal waves. Keep it simple. Archives

May 2024

Categories |

RSS Feed

RSS Feed

|

Privacy Policy • Copyright © 2024 CUbroadcast

|